OVERVIEW

The Coronavirus Aid, Relief, and Economic Security Act (CARES Act), enacted in late March, offered provisions related to distributions from tax-advantaged retirement accounts. Specifically, the goal is to enable Americans to have advantageous access to cash to help sustain them during periods they may not be able to work due to the coronavirus. While COVID-19 has, in some way, affected nearly everyone in the United States, Americans must meet eligibility requirements to take advantage of CARES Act provisions. Specifically, they must be impacted in one of the following ways:

- The retirement account owner, spouse or a dependent is diagnosed with COVID-19

- The account owner experiences adverse financial consequences due to the coronavirus, such as:

- Quarantined

- Furloughed

- Laid off

- Work hours reduced

- No access to child care

- Place of business has closed or reduced hours (including for self-employed)

Taxpayers affected by COVID-19 can take distributions from their IRAs of up to $100,000 and avoid the extra 10% penalty tax. Participants in employer-sponsored qualified plans may also be able to access up to $100,000 of that money if the plan administrator permits. The law permits individuals to self-certify that they meet at least one of the criteria, and plan administrators are authorized to accept the certification unless they have knowledge otherwise. Even if the plan administrator accepts the certification, the account owner may still be subject to normal tax penalties if it is later discovered that he or she did not qualify for the coronavirus-related distribution tax treatment.1

REQUIRED MINIMUM DISTRIBUTIONS

Any seniors who lost invested assets due to market volatility this year can rest easy that they needn’t be permanent losses. By suspending required minimum distributions (RMDs) for 2020, the CARES Act gives retirement plan owners time for their investments to recover — nearly two years if they delay their next RMD until December 2021. The economic setback caused by the COVID-19 outbreak has put many households in financial jeopardy. Learn how recent legislation has eased rules that allow Americans to withdraw money from retirement accounts. This provision applies to certain defined contribution plans and IRAs, including 401(k), 403(b), governmental 457(b) accounts, SEP IRAs, SIMPLE IRAs and traditional IRAs. Beneficiaries who would normally be required to take distributions from inherited IRAs also may skip this year’s distribution when calculating their five-year distribution period.2

Note that if you had already taken an RMD in 2020 after Jan. 31 and don’t actually need the money, the amount may be rolled back into a qualified account on or before July 15.3

EARLY DISTRIBUTIONS

There are two ways to withdraw money from an employer-sponsored retirement plan: as a loan or as a distribution. A distribution is considered a permanent withdrawal that requires income taxes paid in the year withdrawn.

Retirement account owners who qualify for a coronavirus-related distribution have until Dec. 30, 2020, to make a distribution. The total aggregate limit is $100,000 from all plans and IRAs during this time. This particular distribution also waives the normally mandatory 20% income withholding requirement, so account owners may receive the full amount requested.

Retirement account owners who no longer work for an employer are free to take a distribution. However, current employees may take a distribution only if the employer plan allows for hardship or in-service distribution provision. However, the CARES Act does permit employers to make the special COVID-19-related distributions described earlier to eligible employees.

One feature that makes this distribution different is that it waives the standard 10% tax for early distributions by account owners younger than age 59½. While you do have to pay regular income taxes on the amount withdrawn, taxes owed may be spread out evenly over three years.4 For example, if you withdraw $18,000 in 2020, you can report the full amount as income on your 2020 tax return, or, you can claim $6,000 each year on your 2020, 2021 and 2022 returns. By spreading out the tax liability, there’s less likelihood that the extra income will bump you into a higher tax bracket.

DISTRIBUTION REPAYMENT OPTION

One way to avoid paying income taxes on a coronavirus-related distribution is to pay that amount back to an eligible retirement plan. While you must pay income taxes on a coronavirus-related distribution, you can recover those taxes by repaying the distribution within three years after the date you received the distribution. To do so, you’ll need to file an amended return in which you claimed the 2020 distribution as income (up to three amended returns).5

LOAN OPTION

The second way to withdraw money is through a loan, but only if your employer permits loans from the company-sponsored retirement plan. A loan is temporary; you are required to pay that money back to your account within a specified time period. Typically, a retirement account loan is limited to $50,000 or 50% of the account balance, whichever is less.

The CARES Act now allows you to borrow up to 100% of your vested balance or $100,000, whichever is less. Beware that this provision is available only for 180 days after the Act was passed (March 27, 2020).6

LOAN REPAYMENT RELIEF

If you take money out as a loan, you don’t have to report it as income and thus can avoid paying income taxes on the borrowed amount. As you repay the loan, the payments you make are after-tax instead of pre-tax. You’ll also have to pay the loan’s interest charges, but all repayments of principal and interest go back into your account.

One big caveat is that if you don’t pay that loan back in the required time period, you’ll owe income taxes on the outstanding balance as well as a 10% early withdrawal penalty if you are under age 59½.

“If you don’t qualify for a CARES Act withdrawal and you are able to make repayments, a 401(k) loan may be a better option than a traditional hardship withdrawal, if it’s available.”7

DISTRIBUTION OR LOAN?

The main advantages of the CARES Act provisions are that you can avoid penalties and spread out your income tax liability on withdrawals. However, you may wonder whether it’s better to take an early distribution or a loan from your retirement account.

First find out if your plan allows a loan or distribution. If you are already close to retirement, a distribution may make sense since you can avoid the early withdrawal penalty and spread out federal income taxes over a three-year period. If you have plenty of time until retirement, you may want to opt for a 401(k) loan instead. This enables you to avoid taking a large chunk of your nest egg out permanently, which could hurt your long-term accumulation. A loan also permits you to avoid paying taxes altogether, and the interest you pay back to the account can help offset gains lost while your money wasn’t growing.

Bear in mind, however, that if you leave your current job for any reason — including a layoff — you’ll either have to repay that loan or pay income taxes and a 10% penalty if you’re under age 59½.

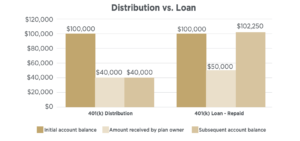

The accompanying graph illustrates the advantage of a loan over a permanent distribution. This hypothetical scenario assumes a $50,000 withdrawal from a 401(k) with a vested account balance of $100,00. The distribution includes the impact of a 20% tax withholding (-$10,000); the loan includes the impact of a 4.5% interest charge added to repayment (+$2,250). Assuming no other contributions were made and the amount borrowed was repaid in due time, the loan option yields $102,250 while the distribution permanently reduces the account by $60,000.

It’s usually best if you don’t have to take money in any form from your retirement accounts, so consult with your financial advisor to review other options before taking this step. If you do decide to withdraw assets, consider these tips:

- Pay off your loan in full and on time.

- Avoid borrowing more than you need.

- Continue saving for retirement — some plans now allow you to continue contributing to a company plan even with an outstanding loan; if not, you can contribute to an IRA.

FINAL THOUGHTS

Remember that the deadline for filing your 2019 tax return has been delayed to July 15. If you need more time, you can file for an extension and pay the amount of tax you expect to owe by July 15 in order to avoid penalties for late filing. Since taxpayers don’t have to file until that date, the deadline for 2019 contributions to IRAs and health savings accounts (HSA) also has been extended to July 15.

If you pay estimated quarterly taxes, scheduled payments for April 15 and June 15 may be delayed until July 15 as well.8

Bear in mind that the COVID-19 pandemic is not over yet, and many scientists predict the likelihood of a resurgence in the fall that could once again put parts of the country under lockdown. Now is a good time to speak with your financial and tax advisors to develop a plan should you need to tap retirement accounts for income later in the year.

1 Ben Steverman. Bloomberg. March 26, 2020. “Coronavirus Shock Is Destroying Americans’ Retirement Dreams.” https://www.bloomberg.com/ news/articles/2020-03-26/coronavirus-shock-is-destroying-americansretirement-dreams. Accessed May 27, 2020.

2 Social Security Administration. “OASDI and SSI Program Rates & Limits, 2008.” https://www.ssa.gov/policy/docs/quickfacts/prog_highlights/ RatesLimits2008.html. Accessed May 27, 2020.

3 1Stock1.com. 2019. “S&P 500 Index Yearly Returns.” http://www.1stock1. com/1stock1_141.htm. Accessed May 27, 2020.

4 Social Security Administration. “Effect of Early or Delayed Retirement on Retirement Benefits.” https://www.ssa.gov/OACT/ProgData/ar_drc.html. Accessed May 27, 2020.

5 Julia Kagan. Investopedia. July 31, 2019. “Sequence Risk.” https://www. investopedia.com/terms/s/sequence-risk.asp. Accessed May 27, 2020.

1213541 – Investment advisory services offered only by duly registered individuals through AE Wealth Management, LLC. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. Neither AEWM nor the firm providing this report provides tax or legal advice. All individuals are encouraged to seek the guidance of a qualified tax professional. Neither AEWM nor the firm are endorsed by or affiliated with the U.S. government or any governmental agency.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Any references to protection benefits, safety, security and lifetime income generally refer to fixed insurance products, never securities or investment products.

The information and opinions contained herein provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management. This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.